Category: Marketing Strategy

-

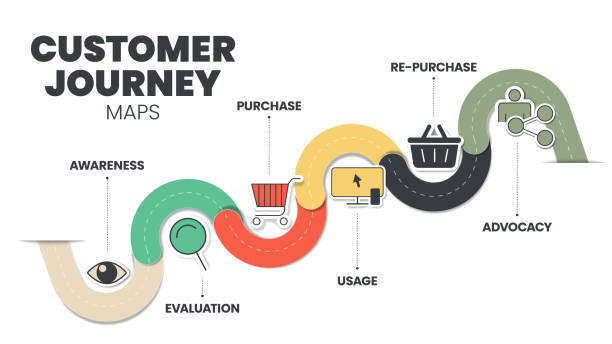

Customer Journey Map

What is a customer journey map? A customer journey map (CJM) is a visual representation of the different stages and touchpoints a customer goes through while interacting with a business or brand. It provides a comprehensive understanding of the customer’s experience, highlighting their needs, motivations, pain points, and overall satisfaction with the brand. CJMs are…

-

Market-driven Organisational Change

Market-led organizational change refers to the process of reorienting a company’s activities and strategies to meet the needs and demands of its customers and the wider market. The concept of market-led change has gained prominence in recent years as companies have recognized the importance of putting the customer at the center of their operations. This…

-

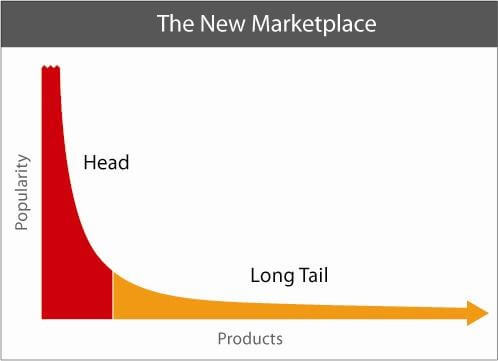

Long tail concept

Zipf’s law states that if a collection of items is ranked by popularity the second item will have around half the popularity of the first one and the third item will have about a third of the of the popularity of the first one and so on.

-

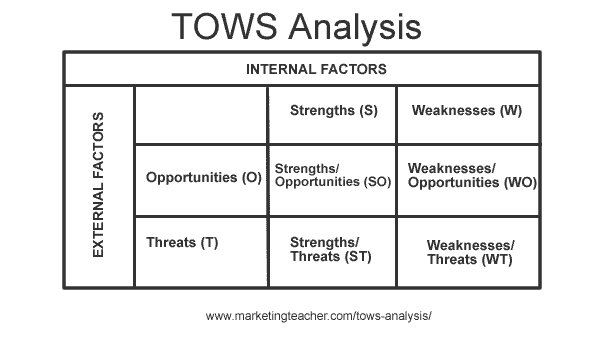

TOWS Analysis

What is TOWS Analysis? TOWS analysis is a tool which is used to generate, compare and select strategies. Strictly speaking it is not the same as SWOT analysis, and it is certainly not a SWOT analysis which focuses on threats and opportunities. This is a popular misconception. TOWS may have similar roots. TOWS is a…

-

Marketing Teacher’s Strategy Page

Marketing Teacher’s strategy page is an internal portal to well known to for strategy such as Ansoff’s Matrix, The Boston Matrix, Porter’s Generic Strategies, Bowman’s Strategy Clock and Gap Analysis.

-

Value Curves

The term value curve appears in three key Harvard Business Review articles by W. Chan Kim and Renee Mauborgne, as well as their 2005 book – Blue Ocean Strategy. The value curve is a tool for strategic managers to see visually how their strategy works in relation to close competitors.

-

Value Chain Analysis

The value chain is a systematic approach to examining the development of competitive advantage. It was created by M. E. Porter in his book, Competitive Advantage (1980). The chain consists of a series of activities that create and build value. They culminate in the total value delivered by an organisation.

-

Shell Directional Policy Matrix

The Shell Directional Policy Matrix is another refinement upon the Boston Matrix. Along the horizontal axis are prospects for sector profitability, and along the vertical axis are a company’s competitive capability. As with the GE Business Screen the location of a Strategic Business Unit (SBU) in any cell of the matrix implies different strategic decisions.

-

Pareto Principle

Pareto principle The Pareto principle is also known as the 80/20 rule. From your own experience you may have come across it, for example 80% of our business comes from 20% of our customers. The principle itself states that 80% of the effects come from 20% of the causes. Let’s look at this in a…

-

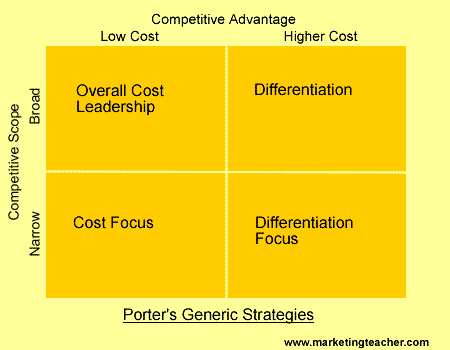

Generic Strategies

Generic strategies were at their most popular in the early 1980s. They outline the three main strategic options open to organization that wish to achieve a sustainable competitive advantage.

-

The General Electric Business Screen

The General Electric Business Screen was originally developed to help marketing managers overcome the problems that are commonly associated with the Boston Matrix (BCG), such as the problems with the lack of credible business information, the fact that BCG deals primarily with commodities not brands or Strategic Business Units (SBU’s), and that cashflow if often…

-

Gap Analysis

Gap analysis is a very useful tool for helping marketing managers to decide upon marketing strategies and tactics. Again, the simple tools are the most effective. There’s a straightforward structure to follow.

-

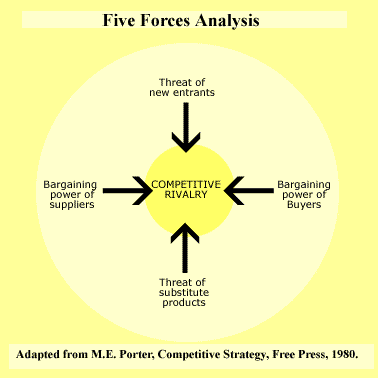

Five Forces Analysis

Five Forces Analysis helps the marketer to contrast a competitive environment. It has similarities with other tools for environmental audit, such as PEST analysis, but tends to focus on the single, stand alone, business or SBU (Strategic Business Unit) rather than a single product or range of products.

-

Bowman’s Strategy Clock

The ‘Strategy Clock’ is based upon the work of Cliff Bowman (see C. Bowman and D. Faulkner ‘Competitve and Corporate Strategy – Irwin – 1996). It’s another suitable way to analyze a company’s competitive position in comparison to the offerings of competitors.

-

Boston Matrix

Like Ansoff’s matrix, the Boston Matrix is a well known tool for the marketing manager.

-

Benchmarking

Benchmarking relies upon a comparison between the activities of your own organization and those of another. Originally benchmarking was used in manufacturing operations where one process could be compared and contrasted with another.

-

Balanced Scorecard

The Balanced Scorecard is an approach that can be used by strategic marketing managers to control, and keep track of, key performance indicators. In fact the scorecard itself is designed to be wholly strategic since it contains long-term outcomes and drivers of success. There are four zones in a balanced scorecard namely financial, customers, business…

-

Ansoff’s Matrix – Planning for Growth

Ansoff’s matrix offers strategic choices to marketing managers. Ansoff’s has four main categories.

-

The Arthur D Little (ADL) Strategic Condition Matrix

Although now slightly dated at first glance, The Arthur D Little (ADL) Strategic Condition Matrix offers a different perspective on strategy formulation. ADL has two main dimensions – competitive position and industry maturity.